July 11, 2026

We Analyzed 36,870 Investment Adviser Firms From SEC IAPD — Here's the 2026 Landscape

We pulled 36,870 active adviser firms from the SEC's IAPD database with our own IAPD scraper and analyzed the industry's geography, disclosure rates, and naming patterns.

Key numbers:

| Metric | Value |

|---|---|

| Unique firms in the dataset (by CRD) | 36,870 |

| SEC-registered (801-) / exempt (802-) / state-registered | 16,759 / 5,091 / 15,020 |

| Firms with a disclosure on record | 9.7% (state range: 6.8%–18.8%) |

| Single-location firms | 71.4% |

| Foreign-headquartered firms | 2,479+ (UK, Canada, Hong Kong lead) |

How we collected the data

We ran 20 keyword searches against IAPD (terms like "capital", "wealth", "advisors", "management") using the SEC investment adviser scraper, filtered to active registrations, and deduplicated by CRD number — every firm's unique regulatory ID. For the four highest-frequency terms, we completed coverage with per-state queries against the same public API, so US results are complete for all 20 terms — no truncation. Foreign-headquartered firms for those four terms come from a bounded search window, so foreign counts are a floor. This is a large sample of firms whose names contain common industry words, not a full census of every registrant. Collected July 2026.

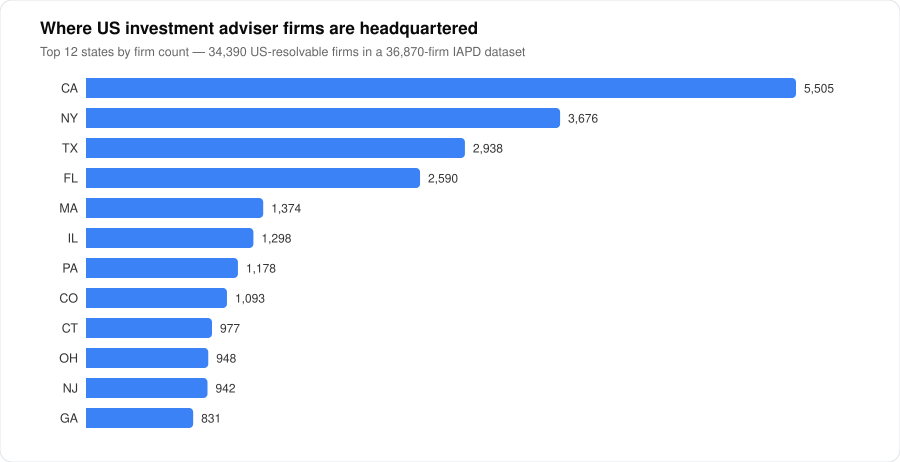

Where adviser firms are headquartered

California leads with 5,505 firms in the dataset, ahead of New York (3,676), Texas (2,938), and Florida (2,590). The long tail matters more than the podium: those four states together hold about 43% of US-resolvable firms, meaning the majority of the industry operates from everywhere else — Connecticut, Ohio, and Georgia each host more adviser firms than most people would guess.

Another 2,479 firms are headquartered outside the US, led by the United Kingdom (594), Canada (205), Hong Kong (199), Singapore (160), and the Cayman Islands (124) — non-US managers registering to touch US clients or markets.

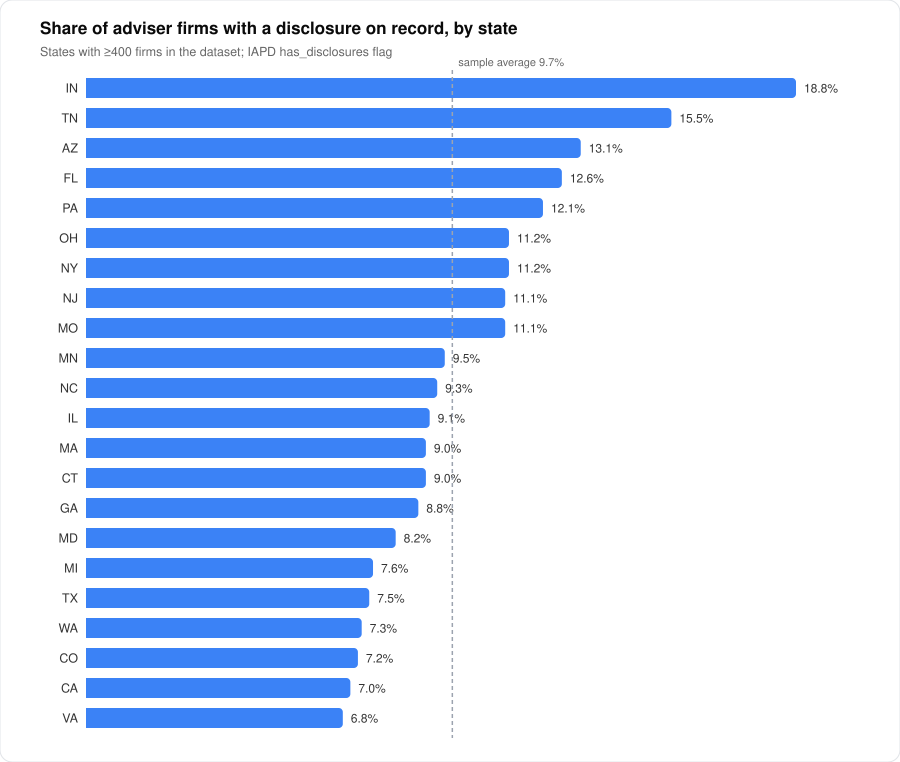

One in ten firms carries a disclosure — and the state spread is nearly 3×

9.7% of firms in the dataset have the IAPD disclosure flag set — the marker for reported regulatory, criminal, or civil events. The spread by state is wider than we expected: among states with at least 400 firms, Indiana (18.8%) and Tennessee (15.5%) top the table, with Arizona (13.1%) and Florida (12.6%) behind them, while Virginia (6.8%), California (7.0%), and Colorado (7.2%) sit at the bottom. An Indiana firm in this dataset is nearly three times as likely to carry a disclosure as a Virginia one — though note the leaders are smaller samples (415 and 452 firms) than giants like California (5,505).

We flag the correlation, not a cause: state-level differences mix firm age, firm type, and enforcement intensity. The interesting part is that the gap exists at all — due-diligence screens that treat "has a disclosure" as a uniform base rate are miscalibrated by geography.

The 112 firms with "family office" in their registered name run above average at 11.6% — for all the exclusivity of the branding, their disclosure rate looks like everyone else's.

Mostly small: 71% of firms are single-location

For an industry managing trillions, the shape is strikingly local: 71.4% of firms report a single office location, and only about 3% report ten or more branches. The registered-adviser industry is a long tail of small shops around a handful of national networks.

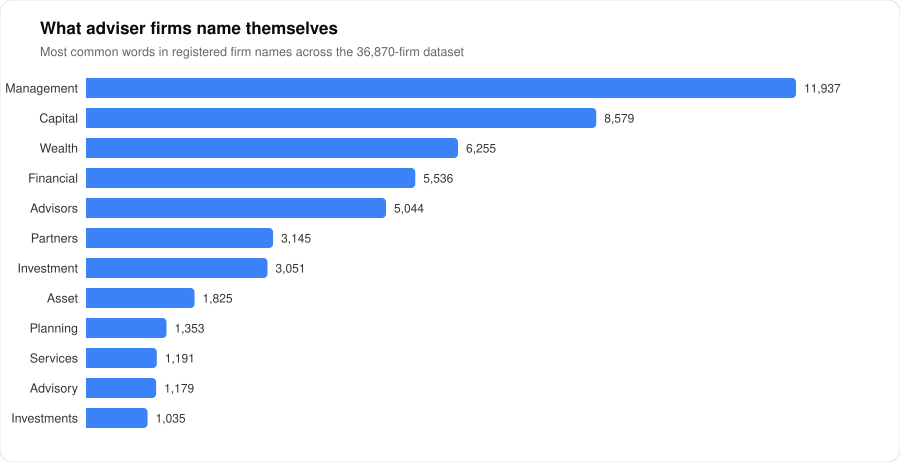

What advisers name themselves

"Management" appears in 11,937 firm names — roughly one of every three in the dataset. "Capital" follows at 8,579 and "Wealth" at 6,255. The naming grammar of the industry is remarkably narrow; if you're naming a new RIA and want to be findable, the data argues for almost any word other than these five.

Reproduce or extend this dataset

Everything above comes from public IAPD records via the SEC investment adviser scraper — search any keyword, get structured firm records (CRD, SEC number, address, disclosure flag, branch count), priced per record retrieved. Pair it with the FINRA BrokerCheck scraper for individual-level records, or see the full playbook in How to Get Company Registry Data in Bulk.

If you use these numbers, cite this page — and if you want a cut we didn't run (by city, by name pattern, by registration type), the dataset takes under an hour to rebuild from scratch.